The Companies Commission of Malaysia (“SSM” or “the Registrar”) has successfully implemented the Companies Act 2016 (“CA 2016”) and the Companies Regulations 2017 (“CR 2017”) in January 2017.

Following the successful implementation of this legislation, Kensington Corporate Services (Malaysia) Sdn. Bhd., a management services company in Malaysia, is well-positioned to assist you with the incorporation and administration of your company.

This document outlines the process for setting up private companies limited by shares in Malaysia.

TYPES OF REGISTERED COMPANIES

- Limited by shares, either be a private company or a public company;

- Limited by guarantee, shall be a public company;

- Unlimited companies, either be a private company or a public company.

REQUIREMENTS OF PRIVATE COMPANIES LIMITED BY SHARES IN MALAYSIA

- Name of company

For private company, the name shall end with the word “Sendirian Berhad” or the abbreviation “Sdn. Bhd.”. - Director

Minimum one (1) natural person who is at least eighteen (18) years of age and shall ordinarily reside in Malaysia by having a principal place of residence in Malaysia. - Member

Minimum one (1), either natural person or corporate body, Malaysian or foreigner. - Single Director / Member

A company may be incorporated with only one (1) member and that single member can also be the sole director of the company. - Share Capital

Minimum one (1) share issued at the price determined by the director(s). - Registered Office

Maintain a registered office in Malaysia to which all communications and notices may be addressed and which shall be open and accessible to the public during ordinary business hours. - Company Secretary

At least one (1) natural person of at least 18 years of age and a citizen or permanent resident of Malaysia who shall ordinarily reside in Malaysia by having a principal place of residence in Malaysia. The secretary shall meet the qualifications as prescribed in the CA 2016. - Constitution

A company, may or may not have a constitution. Without its own constitution, the company, each director and member shall have the rights, powers, duties and obligations as set out in the CA 2016. Based on the CA 2016, a company shall not be formed for any unlawful purpose. Hence, if a company has adopted its own constitution, object clauses are now less significant and may or may not be specified in the Constitution. - Beneficial Ownership

A BO is a natural person who ultimately owns OR controls over a company and includes a person who exercises ultimate effective controls over a company. All newly incorporated companies are required to obtain and file the BO information within 60 days after the appointment of first company secretary.

CORPORATE INCOME TAX IN MALAYSIA

- Companies with a paid-up capital of up to RM2.5m at the beginning of the basis period, gross business income not exceeding RM50milion and foreign ownership (direct or indirect) not more than 20% of the company’s paid-up capital.

Chargeable Income W.e.f YA 2025

The First RM150,000 15%

RM150,001 to RM600,000 17%

In excess of RM600,000 24%

- Other companies that do not meet the above criteria : 24%

- Non-resident company / branch : 24%

ANNUAL OBLIGATIONS OF PRIVATE COMPANIES LIMITED BY SHARES

- Annual Return

File with the Registrar each calendar year not later than thirty (30) days from the anniversary of its incorporation date. - Financial statements and reports

Financial statements and reports are to be circulated to members of the Company within six (6) months of its financial year end. A copy of the financial statements and reports shall be lodged with the Registrar within thirty (30) days from the circulation to its members. For audit exemption companies and exempt private company, please refer to the below sections. - Annual Tax Return

Under the self-assessment system, submission should be made within seven (7) months from the end of the accounting period of the company which constitutes the basis period for the year of assessment. - Annual beneficial ownership confirmation

The company is required to send out notices pursuant to Section 60C at least once in a calendar year to the member for confirmation of beneficial owner information for the purpose of submission of annual return.

AUDIT EXEMPTION OF PRIVATE COMPANIES IN MALAYSIA

Based on the CA 2016, the Registrar may exempt any private company from having to appoint an auditor according to the criteria and conditions set.

Qualifying Criteria for audit exemption -

1. Annual Revenue

- The company’s annual revenue during the current financial year and the immediate past two (2) financial years does not exceed RM3,000,000.

2. Total Assets

- The company’s total assets in the current statement of financial position and the immediate past two (2) financial years do not exceed RM3,000,000.

3. Number of Employees

- The number of employees at the end of the current financial year and the immediate past two (2) financial years does not exceed 30.

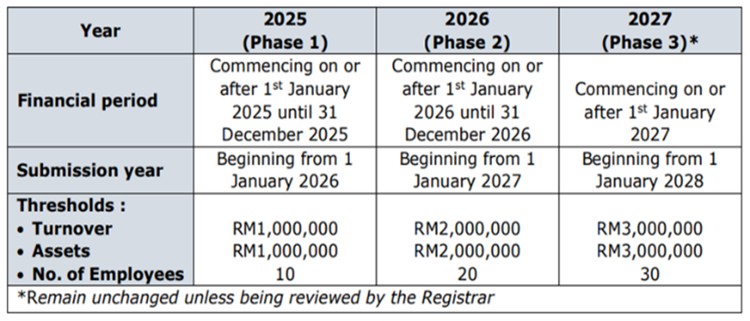

The threshold criteria for audit exemption will be implemented via a phased approach over a period of three (3) years, as shown below:-

EXEMPT PRIVATE COMPANY IN MALAYSIA

Based on the CA 2016, “exempt private company” means a private company:

- where beneficial interest of shares in the company are not held directly or indirectly by any corporation ie. no corporate shareholder; and

- which has not more than 20 members none of whom is a corporation

If a private company fulfils the above definition of exempt company, it has the option of filing an exempt certificate to the Registrar instead of the full audited financial statements. The exempt certificate provides information that -

- The company is and has at all relevant times been an exempt private company;

- A duly audited financial statements and reports required under the CA 2016 has been circulated to its members; and

- As at the date to which the financial statements has been made up, the company appeared to have been able to meet its liabilities as and when the liabilities fall due.

Disclaimer:

Kensington Corporate Services (Malaysia) Sdn. Bhd. is not a licensed tax agent. The information provided in this document is for general reference purposes only and does not constitute legal, tax, or professional advice. You are advised to consult with qualified legal or tax professionals for specific guidance related to your business.