Trusts can play an important role in wealth management for individuals and families, particularly in the area of estate planning.

Examples of typical arrangements and an outline of the formation and administrative procedures involved are detailed below.

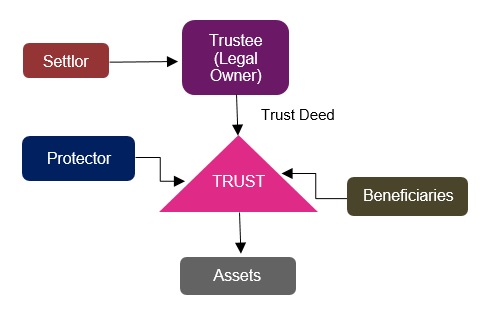

TRUST DEFINITIONS

“Trust” is a legal relationship normally constituted by a written document known as the “trust deed”, which binds the trustee to deal with assets transferred into trust for the benefit of specified beneficiaries.

Settlor” is a person or company who transfers legal title of specific assets to the trustee. This transfer is effected under the terms the settlor and trustee have agreed and which are documented in the trust deed.

“Trustee” is a person or company who becomes the legal owner of the assets transferred into trust without obtaining the right of economic enjoyment of those assets. A trustee is responsible for the administration of the trust in accordance with the terms set out in the trust deed and the law governing the trust. A trustee is under a fiduciary obligation to administer the trust in the best interests of its beneficiaries.

“Beneficiary” is a person or company who has equitable title to the assets held in trust and the right to benefit from them. A settlor may be included among the beneficiaries of a trust.

“Protector” is a person or a company appointed to monitor activities of the trustee on behalf of the beneficiaries and offer guidance to the trustee as the personal circumstances of beneficiaries evolve. The powers, duties and obligations of the protector are defined in the trust deed and are specific to a particular trust. The protector will normally play a fiduciary role with obligations to the beneficiaries and not the settlor.

BENEFITS AND USES OF TRUST

Preservation of Family Wealth

Trusts may be used to own specific assets, such as land or shareholdings in family companies, which a settlor might not wish to divide between descendants or family members. The use of a trust enables individuals to benefit from the assets without being directly interested in these assets. In addition, a trust can effectively protect family assets from the spendthrift behaviour of one or more members of the family.

Immigration / Emigration

Relocation from one country to another, whether this involves an individual, members of their family or the entire family, is often an ideal time to establish a trust or take advantage of any relevant tax, exchange control or other laws of the countries concerned.

Forced Heirship

In some countries there are legal provisions covering the manner in which a person may distribute their assets on death. These provisions can specify the relationship that must exist between the donor and the recipient(s) – for example child, spouse or parent – and the extent to which each party is permitted to benefit. A person who believes such laws might force him or her to act contrary to his or her own wishes may consider transferring their assets into a trust.

TYPES OF TRUST

Many trust arrangements are broadly similar although each is specifically tailored to meet the individual requirements of the settlor and beneficiaries. There are various types of trust, the choice of which will depend upon the circumstances of the settlor and the manner in which it is intended to benefit the beneficiaries.

Common types of trust include:

- Discretionary trust

- Fixed interest trust

- Accumulation and maintenance trust

- Purpose trust

- Reserved powers trust

Discretionary Trust

The most common form of trust is a discretionary trust. The trustee is afforded largely unfettered discretion to exercise his or her own judgement as to the timing, manner and amount by which beneficiaries of the trust might benefit from trust assets.

A discretionary trust might be particularly useful where, at the time of the creation of the trust, the needs of an individual beneficiary or class of beneficiaries cannot be predicted. The beneficiaries of a discretionary trust have no legal rights to any particular portion of the trust fund.

It is customary for the settlor to provide guidance to the trustee with regard to the administration of the trust fund by way of a “letter of wishes”.

A letter of wishes is not legally binding on the trustee, although the trustee will generally have regard to it when considering the exercise of discretionary powers. The letter offers guidance to the trustee in respect of its dealings with the trust fund and may be superseded by subsequent letters written by the settlor, as circumstances change.

Fixed Interest Trust

It is possible to create a trust in a fixed form, so that the trustee does not have any discretionary powers over the distribution of trust assets to beneficiaries. A trust deed may specify exactly how and when assets are to be made available to the beneficiaries. For example, the trustee may be required to distribute all of the income of the trust fund to a particular individual during that person’s lifetime. Thereafter, the trustee may be required to distribute the capital of the trust fund in fixed proportions to specific beneficiaries.

It is possible to arrange a combination of fixed and discretionary trusts. A trustee may, therefore, be given discretionary powers regarding distribution for a period of time, after which there is a requirement to distribute the capital of the trust fund in certain fixed proportions.

Accumulation and Maintenance Trust

An accumulation and maintenance trust may be used where the settlor wants to benefit a specific group of relations, for example his or her grandchildren. This type of trust will often be partly discretionary at the outset and later become one where a fixed interest exists.

The trust deed may afford the trustee a discretionary power to distribute the income and/or capital of the trust amongst the minor beneficiaries (or to their parents on their behalf) for the purpose of their maintenance or education up to a specific age. When that age is reached, each child’s specified share of the trust fund will be distributed to him or her, or form a trust fund for that child.

Purpose Trust

A purpose trust is a type of trust which has no beneficiaries, but instead exists for advancing some non-charitable purpose of some kind. In most jurisdictions, such trusts are not enforceable outside of certain limited and anomalous exceptions, but some countries have enacted legislation specifically to promote the use of non-charitable purpose trusts. Trusts for charitable purposes are also technically purpose trusts, but they are usually referred to simply as charitable trusts. People referring to purpose trusts are usually taken to be referring to non-charitable purpose trusts.

Reserved Powers Trust

Should the settlor wish to reserve certain specified powers in relation to the trust fund, eg. to give direction to the trustee as to investment of the trust assets, or the power to appoint or remove a trustee or beneficiary, he or she may set up a Reserved Powers Trust. The extent to which powers can be reserved is dependent on the settlor’s residence and personal circumstances.

CONCLUSION

Trusts are a well-established concept that can offer benefits under particular circumstances for both individuals and corporations who are predominantly focusing on wealth management.